The creditworthiness of a loan applicant has a considerable influence on credit decisions by financial institutions as well as on the interest rate that z. B. for a real estate loan is calculated. Of particular importance for the assessment of creditworthiness by financial institutions are the score values determined by credit agencies such as Schufa and Creditreform.

We inform you about the decisive factors influencing the scoring and tell you how you can actively improve your personal score value.

1. Financing: The relationship between credit scoring and effective interest rate

Credit scoring maps creditworthiness ("credit rating"). Financial institutions will only grant a real estate loan if the score is sufficiently good.

The better the score, the better the prospects of obtaining a loan. The effective interest rate charged by a bank is also significantly influenced by the score value for most credit institutions. The best interest rate for construction financing is only available to loan applicants with very good creditworthiness.

2. How banks perform their credit scoring

Banks use a wide variety of data that goes into the credit scoring they calculate and ultimately into the credit decision. The data included include u. a. Information from previous banking relationships and the score of credit agencies such as SCHUFA and Creditreform.

2.1 The importance of a reference from a credit agency

As part of the initiation of a business relationship, many companies check the creditworthiness of the credit applicant. For this purpose, especially banks, commercial and telecommunications companies regularly obtain information from a credit agency.

The bank's lending decision – not solely dependent on the Schufa score

However, a Schufa report is not the only factor that determines whether a loan will be granted. The assessment of the creditworthiness of a bank customer depends on various factors and is largely at the discretion of the bank. A house bank, for example, will positively appreciate a loan repayment that has gone smoothly in the past.

However, in the standardized construction financing business, banks generally use the results of automated scoring procedures to ensure efficient workflows for loan decisions and processing.

If a credit institution refuses to grant a loan without the applicant being aware that negative features z. B. are registered with the SCHUFA, the prospective credit applicant should ask for the reasons for the credit rejection. It is possible that inaccurate or out-of-date information is stored at SCHUFA, which has a negative impact on scoring.

2.2 The credit agency SCHUFA

SCHUFA is the most important credit agency for private credit customers, as the financial sector maintains particularly close relations with SCHUFA and also holds a majority stake in SCHUFA.

Schufa Holding AG, Wiesbaden (SCHUFA) is a private company organized in the legal form of a stock corporation. The name "SCHUFA" comes from the former company name "SCHUFA e. V. Schutzgemeinschaft fur allgemeine Kreditsicherung". The SCHUFA's goal is to use its services to create "transparency, protection and security" and thus trust between business partners.

The SCHUFA has the most extensive databases of all credit agencies relevant for the credit industry and credit customers. SCHUFA has some 800 million data records on 66.4 million private consumers and 5.2 million businesses. According to SCHUFA, more than 90 percent of the data relating to natural persons contains only positive information.

The majority of the data stored does not come from SCHUFA itself, but is transmitted to the credit agency by its contractual partners. Some information (z. B. from the debtor lists of the local courts) also obtains the SCHUFA itself. Every year, the credit agency receives about 130 million inquiries about the creditworthiness of private individuals and companies.

Owners of SCHUFA are service companies such as banks and trading companies. Credit banks, savings banks, private banks and cooperative banks hold a total of 86.9 percent, other sectors (z. B. trading companies) 13.1 percent of the shares in the SCHUFA.

The storage of data by SCHUFA

On the occasion of a credit discussion at his bank, the credit applicant gives his consent to obtain a SCHUFA report and to pass on certain data to SCHUFA ("Schufa clause"). Without such consent, a loan agreement is regularly not concluded, since SCHUFA information is generally an indispensable part of the credit assessment by a financial institution.

If SCHUFA has received consent, it stores the following data:

- Personal data such as name, date of birth and gender

- the current and previous addresses (from which z. B. also the "moving behavior" is derived)

- Certain business transactions such as leases and loans (term and amounts), opening of checking accounts, credit cards, telecommunications accounts, accounts at brick-and-mortar stores and online retailers

- "deviating payment behavior" (undisputed debts due for which reminders have already been sent, as well as debts decided by the courts)

- misuse of accounts and credit cards

- Information contained in public records, such as affidavits (EV), warrants for the issuance of an EV, as well as the application, opening, rejection or discontinuation of private insolvency proceedings

- Business and condition inquiries

Excluded from the data storage are

- Receivables under 2.000 euros,

- that have been settled within six weeks,

- for which no enforceable title (z. B. an enforcement notice) exists, and

- as far as the claims for the first time after 01.07.Reported in 2012.

The SCHUFA scoring procedure

The SCHUFA calculates a score value for the individual consumers stored with it, which it then passes on to its contractual partners (z. B. banks) available on request. The calculation of a score value is based on a mathematical-statistical procedure that uses empirical values from the past. The determined score value provides information about the probability of a credit default or. the non-fulfillment of a contractual obligation.

Score values can change over time

- Negative entries are deleted after a certain storage period.

- Changes in experience regarding the likelihood of a loan default lead to an adjustment of the scoring calculation.

- SCHUFA recalculates scoring values for consumers at three-month intervals.

The SCHUFA score value is based on the following information

The SCHUFA score is subject to z. B. Is based on the following facts:

- credit utilization within the past 12 months

- Payment problems (for example, delinquency on credit installments, improperly paid bills from mail-order or wireless companies); and

- the length of time credit cards and checking accounts have been used to date.

The details of the score calculation are not published so that there is no possibility of circumventing the scoring procedure.

design of the SCHUFA score value

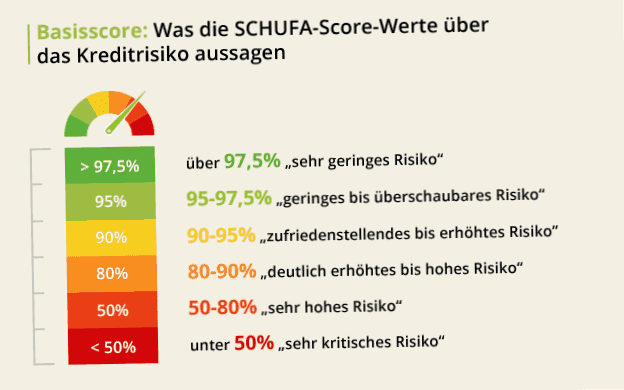

The score for consumers consists of a value between 1 and 100. The score value is an estimate of how likely a consumer is to properly service a loan.

High score values indicate good creditworthiness. If a score value of between 50 and 80 percent is reached, credit decision-makers in banks consider this to be a particularly high credit risk. Below 50 percent, the risk is considered very critical. Credit institutions consider a score of 90 percent to be still satisfactory. Banks usually assume a low risk starting with a score of 95 percent.

Base score and industry score

For consumers (z. B. for private borrowers), a so-called basic score is determined, which is checked and recalculated by SCHUFA every three months.

For the self-employed, freelancers and companies, an industry score calculated on a daily basis that takes into account the specifics of the industry sector in question.

The score for self-employed persons, freelancers and companies includes

- a score value (range 0 to 1.000),

- a ranking level (range A to P; A indicates the best credit rating) and

- the "fulfillment probability" (range 0 to 100 percent).

The automatic deletion of data by SCHUFA

Data is stored at SCHUFA only for a certain period of time. The credit agency then deletes the corresponding data records.

- Inquiries for bank products (z. B. Construction financing; storage period: 12 months)

- repaid loans (storage period: three years to the day after loan repayment or. Termination of the contractual relationship)

- Affidavits and warrants for a PA (three years to the day, or a shorter retention period if the court has proof of expungement)

- Rejection or discontinuation of consumer insolvency proceedings and rejection of a discharge of residual debt (three years to the day)

- Refusal of a discharge of residual debt and cancellation of consumer insolvency proceedings (three full calendar years at the end of the third year)

- Information on debts due (three full calendar years at the end of the year; four full years in the case of non-settled matters)

- Opening of consumer insolvency proceedings (six full years)

- Announcement of residual debt discharges (ten years to the day)

After closing accounts (z. B. Telecommunications or current account), the data will be deleted from the SCHUFA database immediately.

2.3 Other credit reporting agencies: Example Creditreform

Among the numerous other credit reporting agencies that may be of importance to construction lenders' decisions on whether to grant a real estate loan is the Creditreform group of companies.

Creditreform, which also acts as a credit agency and debt collection agency, provides information on private individuals and companies. Creditreform stores almost 80 million data records on over 60 million private individuals. Consumers also have the option of ordering a self-disclosure online from Creditreform.

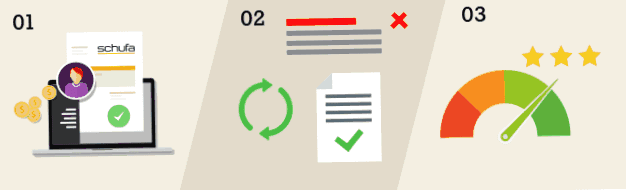

3. Improving creditworthiness – 3 steps to an improved credit rating

If you wish to improve your creditworthiness by correcting the data stored about you, you should proceed as follows.

Step 1: Obtain personal information

First get an overview of the data stored about you.

According to § 34 of the Federal Data Protection Act (BDSG), you have the right to request once a year, free of charge, an overview of the stored data in writing from the storing agency (z. B. SCHUFA) to apply for. You can also request information about the stored data more than once a year, but then at a charge.

A self-report for consumers also lists your current individual basic score (as a percentage value between 1 and 100).

Step 2: Correction or. Deletion of incorrect data

If you notice any errors in the data overview (z. B. outdated or inaccurate entries), you can request correction or deletion. request deletion.

A data correction often improves the personal score value, so that the chances of a positive credit decision by your financial institution and favorable interest rates for a real estate loan increase.

File a written objection to the forwarding and storage of data. As a general rule, write to the company responsible for reporting the now incorrectly stored data to SCHUFA and provide SCHUFA with a copy of this letter.

In your letter of objection, request the correction, blocking or deletion of incorrect data in accordance with §§ 33 ff of the Federal Data Protection Act and justify your objection by explaining the specific circumstances that make certain data appear incorrect.

You can contact SCHUFA as follows:

Postal address Private Clients ServiceCenter:

SCHUFA Holding AG

Private Customer ServiceCenter

P.O. Box 10 34 41

50474 Cologne

Telephone: 0611 – 92 78 0

Fax: 0611 – 92 78 109

The address of the SCHUFA head office (registered office) is:

SCHUFA Holding AG

Kormoranweg 5

65201 Wiesbaden

Sample text for a letter of objection

Request for revocation of an inaccurate data report to SCHUFA

Example of an objection letter to your bank regarding an incorrect Schufa entry. The sample text also contains information on the logical structure of an objection letter. A large part of the content can be used word for word for most cases of objection.

Further measures if bank or SCHUFA refuse to delete data

Especially if you have suffered damage from stored inaccurate records, you should consider whether it makes sense to take further steps to enforce your right to correct the data stored by SCHUFA.

SCHUFA ombudsman

If the review by the SCHUFA ombudsman shows that a consumer has suffered disadvantages as a result of the SCHUFA procedure, the ombudsman will issue an arbitration award, which will result in a rectification z. B. through data correction. If SCHUFA acts correctly, the ombudsman will explain the facts to the complaining consumer in an understandable way. During the ombudsman procedure, the statute of limitations to which consumer claims are subject is suspended.

Involvement of a lawyer

Alternatively, or after an unsuccessful ombudsman procedure, you can call in a lawyer experienced in data and consumer protection law to discuss the prospects of success of further legal action and, if necessary. File a claim in court.

Step 3: Avoid negative entries in the future and positively influence your own score value

You have several options to positively impact your Schufa score. This includes for example,

- Always pay your bills on time.

- Transfer agreed installments for loans, bills for your credit card as well as purchases associated with installments on time.

- Avoid overdrawing a current account or making use of credit in excess of an overdraft facility or credit card credit line that has been granted.

- Make sure that the amount of your income is sufficient to properly service credit claims.

- If you get into financial difficulties, please contact your bank immediately. How you can possibly still avoid a SCHUFA entry.

- Regularly check the data stored about you at SCHUFA. Delete unused current accounts or credit cards. The removal of unauthorized negative Schufa entries improves your score immediately.

4. Conclusion: Regularly check data stored with credit agencies!

Data incorrectly stored by credit agencies (for example, SCHUFA) can also trigger considerable disadvantages in a credit application. It is possible that an application for a construction loan will be rejected by your bank due to a poor score or that you will receive a less favorable loan interest rate.

To avoid such disadvantages, you should at least regularly check your data stored at SCHUFA for accuracy and timeliness by requesting a self-disclosure.