Parents put something aside for education, grandparents save for grandchildren, godparents want their gifts of money to be well invested, etc.

The most common reason to look for an investment for children is probably the later financing of studies or other cost-intensive vocational training.

Find out which savings products are great for saving a nest egg for kids in this article.

This is how expensive it is to study

Investing money early for children definitely makes sense, as five years of study at a German public university including ..

- Accommodation (rent)

- Insurances

- Board

- Tuition fees

- Learning aids etc.

…easily require a total capital requirement of around 60.000 euros.

(1.000 Euro per month x 12 months x 5 years)

Studying at a private university can quickly cost you double that amount. Because tuition alone is 1.000 euros per month.

And whoever wants to go from graduating from an American Ivy League elite university (Harvard, Yale, Princeton, etc.) to a university degree is in the right place.), must also pay an amount of around 60 euros.000 euros.

However per year!

Just as an aside: if the parents earn well, the children are not eligible for Bafog.

However, according to the German Civil Code, they have a claim to maintenance from their parents. This is valid until the first professional training has been completed.

So, let's assume that we have to do it on our own and calculate the said 60€ per child for the studies.000 euros a.

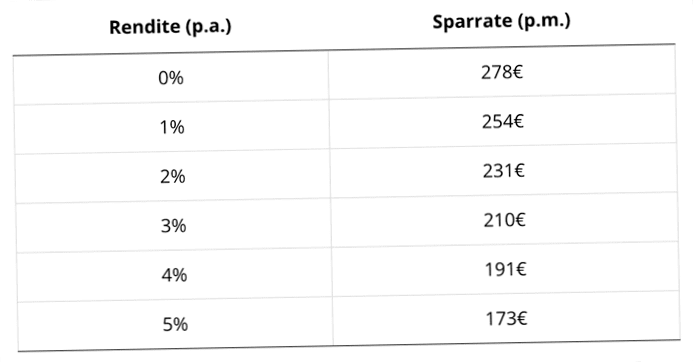

How much you have to save?

This depends partly on the return you earn and partly on your investment horizon.

The ideal case: If you open an account for your baby immediately after birth and pay into it regularly (by standing order), you will have around 18 years to build up your assets.

The monthly savings rate depends on the return:

The bottom line: The higher the return on the paid-in capital, the lower the monthly savings rate required.

With an average real return (after deduction of costs, taxes, and inflation) of 3 percent per year, the monthly savings rate is about the same as the child allowance.

This is currently 204€ per child (for the first and second child).

In other words:

If you "simply" put the child allowance aside every month from birth onwards and achieve a return of 3 percent per year, the savings target (60.000 euros in 18 years) can easily achieve.

What to do if the savings rate is too high?

Of course, you first have to be able to afford to forgo child support in the household budget.

If the savings rate is too high for you, there is no reason to despair.

Even an asset of 30.000 euros should ease the burden on the household budget later.

For this, you simply have to halve the savings target and thus the monthly installments.

And if it is only for 20.000 Euro is enough – by far better than nothing!

Let's not kid ourselves: the biggest sticking point is the necessary 3 percent return on investment.

Saving for children – What hardly pays off

Before we look at how to realize 3 percent return per year ..

…let's first take a look at investment products which, due to a lack of return opportunities, hardly help us when it comes to investing money for children:

- Savings book, savings plan, savings contract

- Daily allowance account

- Time Deposit

- Building savings contract

Savings books, call money accounts and comparable investments have in common that the savings are largely safe thanks to deposit protection.

But none of these savings accounts promises a positive return after deducting inflation in the continuing low-interest phase.

The calculation is simple:

If the interest rate of 1.5 percent (that's the most you can get with time deposits today) is compared with an inflation rate of 1.5 percent ..

…the return is plusminus zero.

In plain language: With "safe" investment products the money does not become more, but at best the purchasing power is preserved.

In the case of savings contracts with a term of several years, the situation is aggravated by the fact that the current low level of interest rates is also fixed for the long term.

Not a good idea.

But even less profitable than a low-interest "children's account" is another financial product ..

Why education insurance is nonsense

The insurance industry likes to lure parents and grandparents with so-called "education insurance" .

A completely pointless and superfluous product category.

Because insurances serve the protection of big life risks and the financing of a study is surely no life risk.

Of course, one could argue that the death of the parents is a risk. Because they are then no longer able to pay for their children's studies.

However, this risk can be easily mitigated by taking out a simple, low-cost term life insurance policy.

This does not require an education insurance!

Which is nothing more than a euphonious euphemism for a high-cost, low-interest savings contract with a long term (aka endowment life insurance).

The best investment for children: equity ETFs

Saving for your children's education with equity funds (ETF savings plans) has three main advantages:

- One obtains an increase in value for the deposited capital (thus 3% real yield p.a. quite feasible)

- The costs are low

- The time investment is low

Instead of buying classic investment funds with high management fees and front-end loads, you should opt for exchange-traded index funds (ETFs).

ETFs track the performance of a stock index – such as the DAX – and are characterized by very low product costs.

Fund savings plans can be set up for a wide range of ETFs at direct banks such as Comdirect, Consorsbank, etc. Set up.

Portfolio for children – an example

Our two children have had their own securities accounts since birth.

Account management is done by us adults in the respective name of the child until the age of majority.

By standing order, we transfer a fixed amount (the children's allowance) every month from our checking account to the clearing account of the "Junior-Depots".

From there, the money is invested in ETF shares at regular intervals (quarterly).

If you want to diversify your risk and benefit from the profits of large companies around the world, an ETF on the MSCI World Index is a suitable investment product.

We have mapped the low-risk part of the portfolio with a call money account.

Minimizing the risk

Of course, an equity investment behaves differently than an interest-based savings contract. In individual years, the return can be quite negative.

Don't forget: The attractive return on the stock market is nothing more than compensation for the fluctuation in value risk that investors have to endure.

We therefore design the asset allocation (division of the portfolio into high-risk and low-risk investments) dynamically.

In other words, the portfolios start with a 90 percent equity exposure, which is gradually reduced to about 50 percent over the planned investment period of 18 years.

This ensures that you have saved enough money at the beginning of your studies that is not (or no longer) subject to the fluctuations in the value of the stock market.

Incidentally, opening an online securities account for your child is not a big problem with the relevant online brokers.

The parents sign the deposit application as legal representatives for the child and attach a copy of the birth certificate to it. The account opening is completed by Postident procedure.

Do the securities accounts actually have to be held in the name of the children? They don't have to, but there are good reasons for doing so ..

Tax treatment of underage accounts and securities accounts

As a newly minted father, I could hardly believe it at the time:

Even before the first diaper pack was used up, we received mail from the Federal Central Tax Office.

Addressed to the baby.

Because every newborn is welcomed by the state as a future taxpayer at an early stage. And thus gets a lifelong identification number according to §139b of the tax code.

It is important to note that children are also entitled to two relevant tax allowances:

- The saver's lump sum (801 euros), and

- The basic tax-free amount (currently 9.168 Euro)

To this must be added the special expenses allowance of 36 euros, so that the tax allowances add up to a total amount of around 10.Add up 000 euros.

Please do not confuse the basic tax allowance with the child tax allowance! This tax allowance is intended for the parents and currently amounts to 7.620 euros per year.

Exemption order and non-assessment certificate

To ensure that no final withholding tax is deducted from the custody account, you should submit an exemption order for the minor's account to the bank.

So that capital income of more than 801 euros per year is not taxed, a so-called non-assessment certificate is required.

This can be applied for at the relevant tax office and is valid for three years at a time.

The certificate must be forwarded to the bank so that no deductions are made for interest income, dividend payments, etc. be made.

However, if the child's capital income exceeds the total allowance of 10.If the taxable income of the child exceeds EUR 000, there is no way around an independent tax return for the child.

This limit will probably only be broken in a few cases ..

Assuming a return of 3 percent and that this is fully subject to the final withholding tax, this would require capital assets (of the child) of over 300.000 euros necessary.

Health insurance pitfall

Children who are co-insured in the statutory health insurance free of charge through a parent may currently "earn" a maximum of 445 per month.

This also includes capital income.

Over the year, the limit is 6.141 euros (12 x 445 euros + 801 euros saver's allowance), which may not exceed.

Otherwise, there is the threat of additional monthly health insurance costs.

Let's move on to a completely different "problem": At the age of 18, custody ends and with it the parental power of disposal over the children's assets.

Which leads us to the next challenge ..

Confidence in financial literacy

In order to be able to effectively use the tax allowances of the children, it makes sense that they generate the capital gains and not the parents.

However, the tax advantage is countered by a danger:

Namely, that the offspring, barely of age, does gross mischief with the carefully accumulated assets. Instead of financing his education.

Sure, the risk exists.

Let's hope that we can teach our "little ones" how to handle money responsibly and the importance of education for their future lives.

Because trust is good, but control is known to be even better, we have decided on the following path ..

Compromise: Split investment

One half of the assets earmarked for education is formed with ETF deposits in the name of the children.

The other half is also invested in ETFs in the fund's own name.

In this way, although we do not benefit to the full extent of the children's tax allowances.

But in return, we also don't take the (full) risk that the "training deposits" will be used to commit fraud later on.

Theoretically, it is possible to transfer back the assets saved in the name of the children before the end of custody.

However, in this case, the investment income earned over the years would have to be taxed by the parents after the fact.

And that is now also not a pleasant idea ..

Finally, a few words about a problem that I'm sure all parents have: How to get kids used to handling bank accounts?

And where to put the pocket money and gifts that accumulate in the piggy bank at home??

Saving pocket money – which account for children?

First of all, when should children start receiving pocket money, how often and how much??

The German Youth Institute makes the following recommendations in this regard:

So much for the recommendations.

In reality, however, the little ones have a much larger budget, at least when monetary gifts are added to pocket money.

Sooner or later, therefore, the question of a savings account for the child arises.

Nowadays, you should not expect significant interest from such a children's account, but at least it should be free of charge.

And it must be "gilt-edged", i.e., it must be impossible for the account to generate a loss.

This is the case with a children's savings account, because ..

Banks keep accounts for minors exclusively on a credit basis. An overdraft facility is therefore not granted.

Differences exist with regard to the provision of cards for withdrawing money from ATMs, (prepaid) credit cards and access to online banking.

A good overview on the topic of children's savings accounts can be found in an article by Stiftung Warentest in this regard.

A practical aspect that can (but does not have to) play a role in the selection: Are cash deposits to the children's account possible?

Alternatively, parents can of course transfer their children's pocket money directly to the account.

Holger founded Zendepot in early 2013, where he was one of the first German bloggers to provide regular information about passive investing with ETFs and other financial topics. In June 2021, Holger decided to close the Zendepot project for himself in order to concentrate on his core business, his own practice. However, Holger's posts can still be found on the Zendepot blog.